Welcome to November… a lot has happened in the last month.

If you’re new here, Workforce Wrap Up aims to give a quick 5-minute download of interesting highlights that happened in our economy in the past month. You can read last month’s Wrap Up here.

Over the past month, we elected a new president, saw signs of an increasingly cooling labor market despite data also indicating a very resilient consumer, and received another rate cut. Given the change in the upcoming administration and increasingly complex geopolitical issues, the only thing that is for certain moving forward is uncertainty.

With that, let’s dig in.

It’s official, we are heading into another 4 years of a Trump administration. The next few months will be volatile as the market aims to get a better handle of what Trump’s fiscal policy will be.

The yield on 10-year US Treasuries increased from 4.29% on Tuesday (Nov 5th) to 4.43% on Wednesday (Nov 6th), reflecting the expectation of higher inflation and interest rates under Trump. The U.S. dollar index also spiked on Wednesday. Both the yield and the dollar have reverted back to normal as of writing this on Friday.

Trump’s agenda includes significant tax cuts that will increase the deficit as well as tariffs which are predicted to drive up inflation if implemented.

Markets were pricing in 1.9% annual inflation over the next five years in early September - it rose to 2.41% as of writing this.

A report by the National Retail Federation found that Trump’s proposed tariffs would reduce American consumer spending power for common household goods by $46 billion - $78 billion per year. Toy prices would rise as much as 56% given the US imports nearly all of its toys, with 77% coming from China.

Unfortunately, lower-income households will disproportionately face the impact of tariffs, as they spend a larger percentage of their income on goods.

Trump’s proposed policies around immigration will also have an impact on the economy. Depending on the policy implemented, Bloomberg predicts material decreases in GDP growth (industries like construction and hospitality will be hit hard due to lack of labor) with slight improvements in inflation due to decreased demand.

Three scholars were awarded the Nobel prize for their research on why some countries prosper while others do not. The answer has less to do with economics and more to do with having a strong societal fabric.

Daron Acemoglu and Simon Johnson of MIT and James Robinson of University of Chicago examined various political and economic systems introduced by European colonizers to understand the connection to a country’s prosperity.

Unsurprisingly, their findings showed that prosperous societies have built institutions that bind its citizens - institutions that allow people to innovate, exchange goods and services, and live peacefully. Successful societies are reliant on courts that decide cases fairly and police who enforce the law.

Societies built on extraction may initially be richer but ultimately fail as they develop institutions that are not able to adapt and innovate over time and do not incentivize people to invest in their own country.

One interesting finding was that density of an area before it was colonized had a significant impact on the type of institutions that were built. In areas that were more densely populated before they were colonized, colonizers built more extractive institutions that focused on benefitting the few elite at the expense of those who were already there. In areas that were more sparse, they were more likely to build institutions that were more fair because they needed to have systems that incentivized settlers to work hard and invest in their new homeland.

Their research found that a pivotal point in time was the industrial revolution. Technical innovations in that time period deeply penetrated parts of the world where places had institutions that had been established for the wider population vs led to a reversal in prosperity in areas that did not.

It obviously seems intuitive that if you build stronger institutions that are trusted and inclusive, a country will have better long-term outcomes. Yet, it is critical to remember that and appropriately adjust as trust in US institutions is at the lowest its ever been.

US job growth slowed considerably in October, with the labor market only adding 12,000 jobs.

The small employment gains were driven by health care and government, with healthcare adding 52,000 jobs and government adding 40,000. Temporary help services declined by 49,000 - it has decreased by 577,000 since its peak in March 2022. Manufacturing employment decreased by 46,000.

It is possible that the data was impacted by Hurricane Helene and Milton as well as strike activity in the manufacturing sector.

The unemployment rate remained unchanged at 4.1 percent.

Average hourly earnings for all employees increased by 0.4 percent or 4% year-over-year.

August and September employment data was revised down by 81,000 and 31,000, respectively.

Layoffs remained stable but job openings continued to decline to pre-pandemic levels.

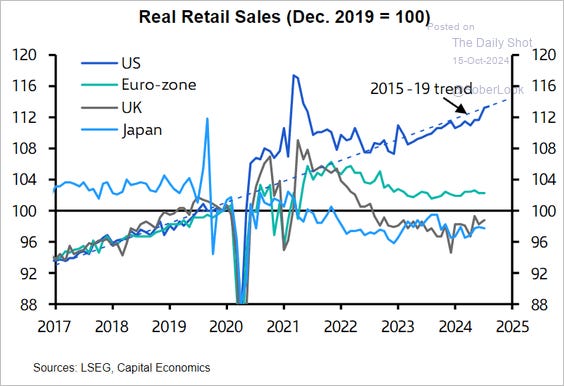

Yet, retail data shows signs of a resilient consumer.

Personal consumption expenditures increased at a 3.7% annualized rate, up from 2.8% in the second quarter.

Most retail categories saw spending increase in September, including clothing shops (+1.5%), restaurants and bars (+1%), and other food shops (+1%).

The US consumer is particularly resilient especially relative to other advanced economies.

Retail foot traffic continues to increase.

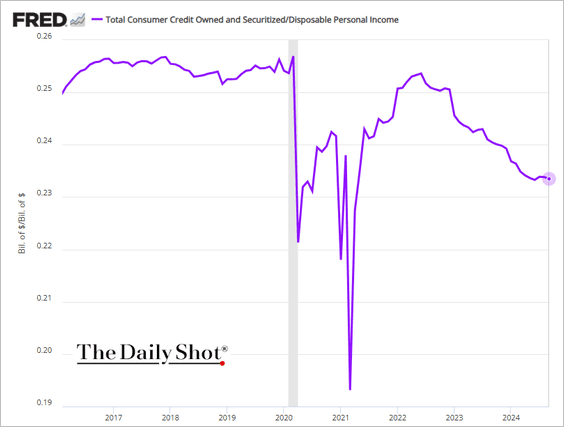

While there is a lot of anecdotal information about a struggling consumer, consumer debt has been declining relative to disposable income.

Global public debt is a serious problem according to the IMF’s latest report.

Global public debt is on track to get to $100 trillion by the end of the year or 93% of global GDP. The IMF estimates it will approach 100% by 2030, with the US and China driving most of the increase.

Now would be the time to rein back spending but the IMF notes given trends like aging populations, geopolitical challenges, and transitioning to greener technology, the reality is that it will lead to more spending and not less.

The upcoming administration’s policy proposals will likely only increase the deficit, not improve it. The latest CBO projections (not accounting for campaign promises) shows debt will get to 122% of GDP by 2034.

Moreover, the world’s 26 poorest economies which have 40% of all people who live on less than $2.15 a day are deeper in debt than at any time since 2006. These countries are increasingly vulnerable to climate related disasters, two-thirds are either in conflict or have difficulty maintaining order because of institutional fragility. Nearly all are commodity-exporting countries that are subject to volatility in demand.

To end on a positive note, the US continues to outperform other advanced economies when it comes to growth.

Despite the shocks of the last few years, including a pandemic, inflation, and geopolitical challenges, the US economy has continued to grow very nicely.

The IMF’s World Economic Outlook projects the U.S. will grow 2.8% this year, which is the fastest growth among the G7 major economies.

This time last year, the IMF projected a U.S. slowdown to 1.5% growth but the U.S. has continued to defy expectations.

IMF’s chief economist says there are two drivers: the first is strong productivity growth which is unlike other advanced economies. The second is a rise in immigration that has supported our labor market.

As always, thank you for reading Workforce Wrap Up! If you have any suggestions on what you’d like to see more or less of, shoot me a note at jomayra@reachcapital.com. Enjoy your Thanksgiving and we will see you back in December.